The Bridge To 2026

Scott Tremlett, CIMA®, CFP®, ChFC® | CEO/Chief Investment Officer

Executive Snapshot

2025 was a year that rewarded patience, punished extremes, and quietly reset expectations. Markets absorbed tariffs, election noise, and a cooling labor market — yet still delivered strong returns, driven overwhelmingly by AI-related capital spending and earnings power. As we head into 2026, the question is no longer whether growth slows, but how much resilience remains once policy support, AI infrastructure spending, and global diversification are fully priced in. I enter 2026 constructive — but selective. Every sector will have its own winners and losers. This is a year where discipline matters, where diversification works, and where the biggest risk may be assuming central banks will rescue markets the way they did in the past. However, dispersion presents an opportunity I can take advantage of.

One of the most important risks heading into 2026 is not macroeconomic—it’s behavioral. Over the past decade, markets conditioned investors to expect rapid action, stability, and backstops. Markets have shown resilience to this point and that explains why policy makers have less urgency, why risk assets remain supported, and why investors should be careful about over-positioning for a recession that continues to be deferred rather than delivered.

Consumer behavior warrants greater emphasis, and overall stability masks the growing inequality. Aggregate spending masked a widening gap between upper-income and lower-income households, with the top end of the consumer continuing to carry the economy forward. That bifurcation is not new, but it became more pronounced in 2025, and it will shape how growth slows—or doesn’t—in 2026. This is not a call for complacency, but it is a reminder that headline indicators often miss where the real strengths and the real stressors actually live.

Section I: 2025 in Review — A Narrow Market with Broad Implications

US equities delivered another strong year in 2025, extending what is now one of the strongest three-year runs outside of the late-1990s tech boom. The headline numbers, however, mask an important reality: performance was heavily concentrated. A relatively small group of AI-linked companies drove the bulk of returns, earnings growth, and capital spending. International equities quietly staged a comeback.

After years of underperformance, valuation discipline, improving earnings trends, and currency dynamics finally aligned. Energy prices fell, inflation stabilized, and rates edged lower — creating a foundation for broader participation going forward. Two years ago, earnings growth for non-AI companies was negative. Last year, AI still led the way, but the gap narrowed.

AI was not a trade in 2025; it was the economy. Capital spending tied to data centers, semiconductors, power infrastructure, and networking accounted for a material share of GDP growth. That matters because it reframes AI from speculation to infrastructure.

Investor behaviors rewarded a narrow group of winners masked the fact that most assets required patience, balance sheet strength, and earnings durability to perform. The key takeaway is that strong headline returns disguised growing internal fragility. When markets reward a small subset of names, investors are tempted to chase outcomes rather than assess probabilities. That tendency raises risk heading into 2026, when dispersion—not momentum—is likely to dominate returns. I’m very mindful of the herd effect surrounding the Mag-7 stocks, and I tend to avoid large allocations to names that are heavily crowded by investors. In my view, mid-cap stocks often offer the most attractive risk/reward profile — but it’s critical to be selective and understand what you own. I’m not suggesting broad mid- or small-cap index exposure, but rather a more targeted approach.

Section II: Federal Reserve Reality — Fewer Cuts, Higher Bar

There is a growing disconnect between market expectations and policy reality. While futures markets continue to price multiple rate cuts, the Fed’s actions—and increasingly its tone—tell a more cautious story. Recent headlines involving the Department of Justice and renewed scrutiny around regulatory independence only reinforce what markets already know: the Fed is operating in a politically noisy, inflation-sensitive environment. Even as inflation moderates, structural forces—tariffs, fiscal expansion, immigration, labor shortages, fiscal deficits, and energy constraints—limit how aggressively central banks can respond to market stress. These all work against a rapid return to 2% inflation.

While inflation cooled meaningfully from its post-pandemic highs, it did not revert to the pre-2020 regime investors had grown accustomed to. Shelter costs, labor constraints, and energy infrastructure bottlenecks remain persistent. For markets, this matters less because inflation is falling and more because it is sticky. Sticky inflation keeps real rates positive, limits central bank flexibility, and raises the bar for aggressive easing.

This backdrop reinforces why I continue to view 2026 as a year where disinflation continues, but normalization does not. Markets expecting a rapid return to ultra-low rates are likely to be disappointed. Instead, the more probable outcome is an environment where inflation fluctuates in a narrow but elevated range—low enough to avoid crisis, high enough to constrain policy.

My base case calls for two rate cuts in 2026, though one cut is well within reason — and it’s not out of the question that the Fed stays on hold altogether. The Fed does not need to rush. Fewer rate cuts are not a policy error, but a constraint. Financial conditions are not restrictive, equity markets are near highs, and AI-driven investment continues regardless of modestly higher rates. This is not a hostile backdrop — but it is not a bailout cycle either.

Section III: Employment — Cooling, Not Cracking (Yet)

The labor market is no longer tight, but it is not broken. Hiring has slowed, quits have declined, and wage growth is moderating.

Importantly, layoffs remain contained outside of select sectors undergoing structural change. Job growth slowed meaningfully in 2025, and 2026 is likely to continue that trend. The key question is pace. A modest rise in unemployment would give the Fed room to maneuver without forcing aggressive action. A sharp rise would change the calculus—but that remains outside my base case.

There are several structural forces at work in the labor market that don’t get much attention but are critical to understanding the full picture. Immigration has slowed, and when the U.S. was absorbing more than 1 million new residents annually, the economy had to generate a significant number of additional jobs to keep pace. If that number falls closer to 250,000 or less, the number of

new jobs required each year declines meaningfully. At the same time, roughly 10,000 baby boomers are retiring every day, another powerful demographic shift that reduces labor supply and, in turn, the number of jobs needed to keep unemployment stable. Those two factors alone influence the unemployment rate and help prevent it from rising too quickly. The broader demographic trend in the U.S. is aging, which keeps the overall participation rate around its long-term average, yet prime-age participation (ages 25–54) remains strong and near its highest levels in decades. There are a lot of moving parts, and it’s important to step back and view the labor market in its entirety rather than focus on just one data point.

Wage growth is also slowing but remains elevated relative to pre-pandemic norms. This dynamic supports consumption at the top end, even as pressure builds for lower-income households. This unevenness reinforces why economic data may continue to send mixed signals throughout the year.

This is what late-cycle normalization looks like, time will tell how it plays out. Employment is a lagging indicator, and while risks are rising, AI-related investment, fiscal spending, and household balance sheets continue to provide a buffer.

The risk for 2026 is not mass unemployment — it is confidence. If consumers begin to feel job insecurity before it shows up in the data, spending could soften quickly. For now, the labor market remains a cautionary signal rather than a warning sign.

Section IV: US Equity Sectors — Leadership Broadens, Volatility Rises

2026 should look different from 2025 at the sector level. While AI remains the dominant force, leadership is expanding beyond the original mega-caps. As valuations reset higher over the past two years, earnings have reclaimed their role as the primary driver of equity returns. Multiple expansion did much of the heavy lifting earlier in the cycle. From here, earnings growth—and the quality of that growth—will determine outcomes. This dynamic favors companies with pricing power, scale, and balance-sheet flexibility. It also explains why dispersion across sectors and regions is likely to increase. Broad beta can still work, but selective exposure matters more in 2026 than it did in the easy liquidity years.

I expect: -Technology to remain a core holding, but with greater dispersion between infrastructure winners and software laggards.

Industrials and Utilities to benefit from data center build-outs, power

generation, and grid modernization. -Financials to stabilize as net interest margins normalize and credit remains contained. -Consumer Staples to remain volatile amid policy uncertainty and margin pressure. Health Care …could go either way.

Even within individual sectors, the gap between winners and losers is likely to widen. My approach is to focus on identifying what I believe will be the sector leaders rather than owning everything indiscriminately.

Volatility, in itself, isn’t necessarily a negative when it comes to diversification. While low correlation is key, pairing low-correlation assets with measured exposure to higher volatility can actually improve risk-adjusted returns. I understand that putting a positive spin on volatility may raise eyebrows, but when selection is disciplined and you’re identifying more winners than losers, volatility can work in your favor rather than against you.

This is a market where targeted sector positioning and active management matter again.

Section V: International Opportunities — Currency, Valuation, and Catch-Up

One of the more underappreciated positives for 2026 is international diversification — particularly in the first half of the year. The case for international investing in 2026 is not just valuation-driven; it is macro-driven.

A less exceptional U.S. growth profile, combined with a Federal Reserve that is closer to the end than the beginning of its tightening cycle, creates room for a softer dollar—particularly in the first half of the year. A softer dollar, alongside lower valuations and improving earnings, has restored international exposure as not just a return enhancer, but a meaningful risk management tool.

A weaker US dollar early in 2026 acts as a tailwind for non-US assets. A weaker dollar historically acts as oxygen for international and emerging market assets. When paired with improving earnings trends abroad and a narrowing growth gap, the risk-reward outside the U.S. improves materially. This does not imply abandoning U.S. assets, but it does argue against home-country bias at a time when diversification is finally being paid to wait. Combined with lower starting valuations and improving earnings trends, this creates a favorable setup for international equities.

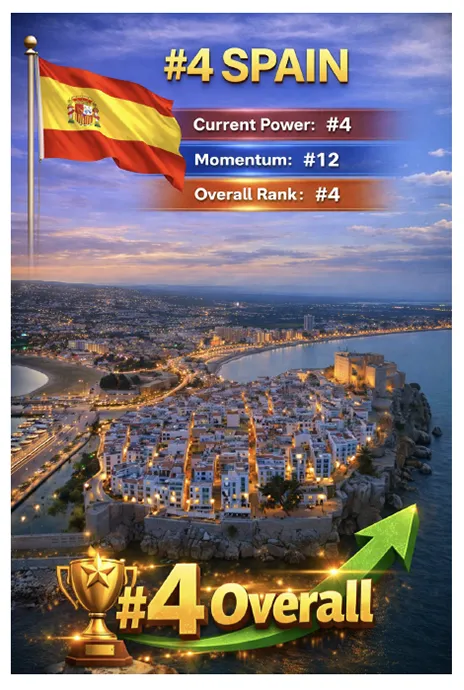

Europe

Europe enters 2026 with low expectations—and that is precisely what makes it interesting. Growth remains modest, but inflation has cooled faster than in the U.S., policy uncertainty has diminished, and corporate earnings appear more resilient than many expected. Energy risks that once dominated the narrative have faded, while fiscal support and improving consumer activity have quietly stabilized the region.

European equities also benefit from sector composition. Industrials, financials, and exporters stand to gain from a stabilization in global trade and a more predictable policy environment. Combined with attractive valuations and improving sentiment, Europe represents a source of return potential that does not require heroic assumptions.

Europe is not booming — but it is stabilizing. Fiscal spending in Germany, easing financial conditions, and AI adoption across industrial, telecom, and energy sectors are quietly improving the region’s growth profile.

Emerging Markets

Emerging markets enter 2026 with several structural advantages. Many central banks tightened earlier and more aggressively than their developed-market counterparts, giving them flexibility as inflation cools. Commodity-linked economies benefit from ongoing infrastructure investment, energy demand, and electrification trends tied to AI and reshoring.

Crucially, currency dynamics matter. A softer dollar eases financial conditions across emerging markets, improves capital flows, and reduces balance-sheet stress. Add improving earnings growth and selective deregulation, and the setup for EM looks materially better than it has in years.

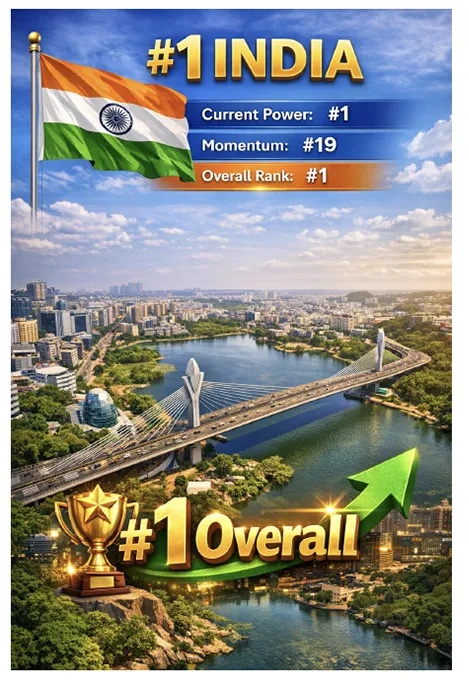

Emerging markets enter 2026 with better inflation control, healthier balance sheets, and exposure to global capex cycles. India, parts of Southeast Asia, and Latin America stand to benefit from supply-chain realignment and AI-driven infrastructure demand.

Paramount Global Rankings

Indonesia ranked #4 but was removed due to lack of liquid markets.

Russia ranked #7 but was removed due to geopolitical issues.

FUN FACTS:

- The Central Bank of Turkey recently CUT rates to 37%

- Australia and Japan recently RAISED rates.

- China, India, Russia, and Turkey recently LOWERED rates.

- 16/20 countries examined are currently OVERVALUED.

Section VI: AI — From Narrative to Infrastructure

Artificial intelligence continues to move from concept to implementation. In 2025, markets rewarded the obvious winners—platforms, hyperscalers, and headline names. In 2026, the focus shifts to the second and third order effects: infrastructure, power, data, and efficiency. AI continues to define this cycle, but the story is evolving. The market is moving past hype and toward monetization.

The most durable opportunities are infrastructure-based AI investments:

- Semiconductors and advanced chip manufacturing- Power generation and grid equipment- Data center construction, cooling, and networking- Industrial automation tied to AI deployment. The buildout required to support AI is massive. Data centers, grid reliability, power generation, and semiconductors all sit upstream of the applications investors see on the surface. This is where capital intensity is highest—and where earnings visibility can be strongest. These are not short-term trades. They are multi-year capital cycles that resemble prior infrastructure booms — railroads, electrification, highways — not dot-com excess. That said, valuation discipline matters. Not every AI stock is an AI investment.

Importantly, AI is not just a technology story; it is a productivity story. While it may take time for that productivity to show up in aggregate data, companies that deploy AI effectively should see margin expansion and operating leverage even in slower growth environments.

This reinforces my emphasis on AI as a multi-year industrial upcycle, not a short-term trade. The biggest investment risk now is confusing technological excitement with durable economics. AI rewards patience, scale, and pricing power—traits more common in enablers than in headlines.

Section VII: Metals & Alternative Assets — The Quiet Diversifiers

Real assets reasserted their relevance in 2025, and that trend carries forward. Energy markets appear structurally oversupplied in the near term, but underinvestment and geopolitical risk keep long-term price volatility elevated. Meanwhile, metals tied to electrification, infrastructure, and AI-driven demand continue to benefit from constrained supply.

Gold proved again in 2025 that it is not an inflation hedge — it is a confidence hedge. In a world of large deficits, geopolitical uncertainty, and central bank balance sheets that never truly normalize, gold and select metals retain strategic relevance.

Copper and aluminum benefit directly from electrification, AI infrastructure, and grid expansion. Alternative assets — particularly private credit and real assets — continue to play an important role as volatility rises and public markets reprice risk.

In a world where deficits remain large and confidence in fiat discipline is uneven, gold and select real assets retain a place in diversified portfolios.

Closing Thoughts

As we move into 2026, the investment landscape is best described as a transition—not a turning point. The nomination of Kevin Warsh as Federal Reserve Chair represents more than a personnel change; it signals a shift toward reinforcing monetary credibility at a moment when markets have begun to question long-term policy discipline. Warsh is widely viewed as more hawkish on balance-sheet expansion and less tolerant of open-ended liquidity support. His appointment suggests an effort to stabilize confidence without abruptly tightening financial conditions. The sharp rally in gold and sustained dollar weakness earlier this year reflected skepticism about the long-term endgame of policy. The swift reversal following Warsh’s nomination — precious metals down, the dollar firmer, equities and rates relatively steady — indicates that markets interpreted his selection as a commitment to restraint and credibility.